to an IRA Without Paying Taxes; Steps, Rules, Taxes and Benefits")

How to Transfer a 401(k) to an IRA: If you are changing jobs or planning to retire, you may face some important retirement savings decisions. A very common question is whether to transfer your 401(k) into an IRA (Individual Retirement Account) or not.

Handling a 401(k) rollover isn’t complicated, but perhaps making the prudent moves can help you dodge taxes, penalty fees, or poor investing decisions. Knowing the ins and outs of the situation will also allow you to help keep track of your money.

What Is a 401(k) Rollover?

A 401(k) rollover is taking money out of a 401 (k) plan that your company has sponsored. This money is then transferred into an IRA. The money will stay invested for pension purposes and, if the rollover is handled properly, you won’t be taxed or penalized for early withdrawal.

Note the difference: a rollover is not a withdrawal of money from your retirement account. A rollover is just transferring your money from one retirement account to another. Moving your money from your IRA to your rollover account isn’t a taxable event and won’t result in early withdrawal penalties, so it is considered one of the safest ways to transfer retirement money after leaving an employer.

Why Roll Over Your 401(k) Into an IRA?

Almost all investors who open an IRA do so because they want to have a lot more options than most employer plans provide.

Fewer Investment Options: Employer 401k plans generally offer fewer mutual funds than employees would choose for themselves.

With an IRA, you can often invest in:

- Stocks

- Bonds

- Exchange-Traded Funds (ETFs)

- Mutual funds

- Certificates of Deposit (CDs)

- Treasury securities

More Control of Your Money: An IRA is yours, and yours alone, not your employer’s. If you change jobs several times throughout your career, your IRA stays with you.

May Have Lower Fees: Certain workplace retirement plans have few administrative fees and relatively low-cost investment funds.

Simpler Retirement Planning: If you are carrying a handful of old 401(k) accounts from various employers, putting those separate savings into a single IRA can be simpler-easier to keep track of and determine the appropriate time to start withdrawing funds in retirement.

Direct Rollover vs. Indirect Rollover

You can use either of two methods to draw on your retirement savings.

Direct Rollover

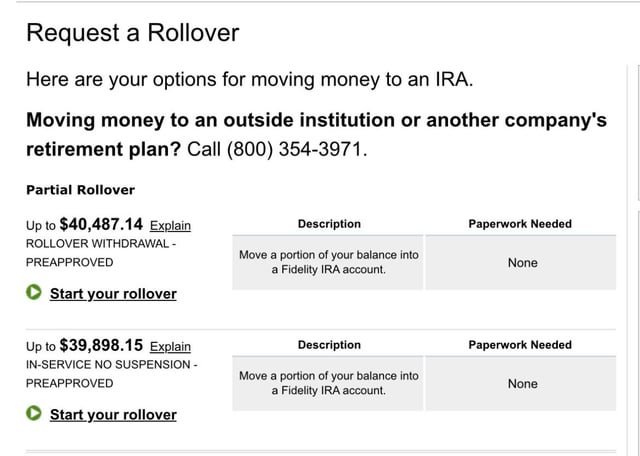

A direct rollover is likely the easiest and safest route. Your current 401k provider will send the money directly to your IRA provider without it ever passing through you.

A direct rollover means your employer’s retirement plan administrator will send the money directly to your IRA provider (bypassing your bank account altogether). As you never take control of the money, there is no 20% tax withholding and no risk of missing an IRS deadline.

Indirect Rollover

In an indirect rollover, you receive the money first, and then have 60 days to deposit it into your IRA. One complication in an indirect rollover is that employers are typically required to withhold 20% of the distribution for federal income taxes.

Remember, though, that if you miss the 60-day deadline to roll over after a distribution, the entire distribution becomes taxable. If you’re under 59, you’ll also probably face a 10% early withdrawal penalty. As you can see, indirect rollovers are much more risky than direct transfers.

Roth and Traditional IRA Contribution Limits Rise for 2026: What Savers Need to Know

How to Transfer a 401(k) to an IRA Without Paying Taxes?

Step 1: Decide Whether a Rollover Is Right for You

Check whether moving your retirement savings makes sense. Before you Rollover, think about: compare your existing 401(k) to what you might find in an IRA. You can consider:

- Investment choices

- Annual fees

- Customer service

- Retirement planning tools

- Access to financial advice

There may still be a handful of cases in which even maintaining your money in your employer’s plan is not a bad idea (if your plan has cheap fees or distinct investment choices).

Step 2: Choose an IRA Provider

Do thorough research on financial institutions before establishing an IRA.

Many investors compare providers based on:

- Investment selection

- Trading costs

- Fund expense ratios

- Mobile and online experience

- Research tools

- Educational resources

- Customer support

Select a provider whose investment approach and retirement planning strategy match your own.

Step 3: Open Your IRA

You’ll need to decide whether to open:

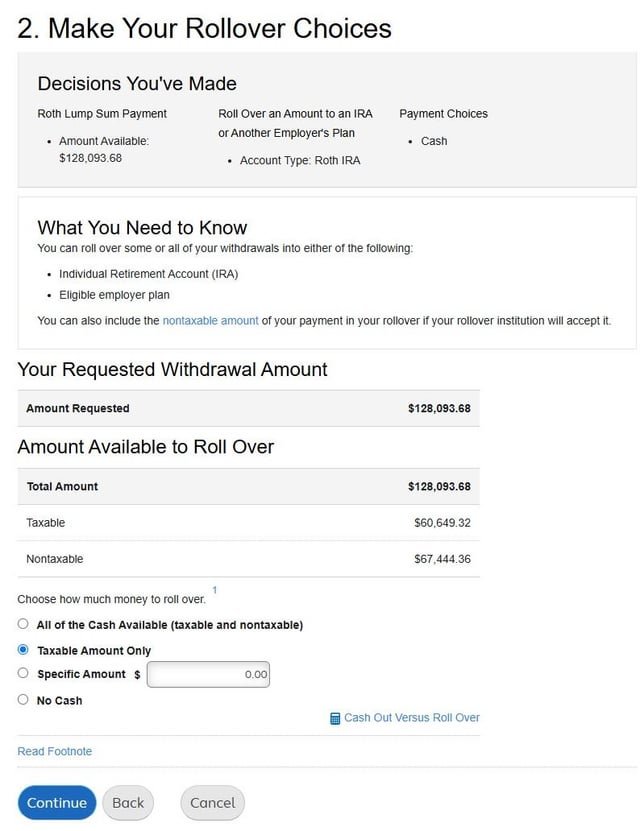

Traditional IRA: This type of account is sometimes a rollover from a typical 401(k) plan. Rolling over a 401(k) to an IRA generally doesn’t cause an immediate tax charge.

Roth IRA: Moving a Traditional 401(k) balance into a Roth IRA is considered a Roth conversion.

Since Roth accounts are funded with after-tax dollars, you’ll normally owe income taxes on the amount transferred in the year of the transfer.

Step 4: Contact Your 401(k) Administrator

Let your plan administrator know you want to do a direct rollover. They’ll give you the documentation and walk you through the transfer.

You may need:

- Your IRA account information

- The receiving financial institution’s details

- Identification documents

- Employer plan information

Step 5: Complete the Transfer

The funds will be deposited directly into your IRA once the paperwork is processed. The time frame depends on the provider, from as long as three to four days up to a few weeks.

Step 6: Invest Your Money

One of the biggest errors is thinking the money is automatically invested once it gets into the IRA. Very frequently, the money has been sitting in a cash/securities settlement account.

Select investments that are consistent with your retirement plan.

Common Mistakes to Avoid

- Missing the 60-day deadline during an indirect rollover.

- Choosing to cash out rather than roll over.

- Failure to invest the money that was transferred.

- Investment fees that are ignored.

- Investing in a way that conflicts with your future objectives.

- Failure to verify beneficiary information at account opening.

Can You Roll Over a Roth 401(k)?

Yes. You can generally roll over a Roth 401(k) into a Roth IRA. Because both accounts are made up of after-tax dollars, the rollover is normally tax-free, given it is done correctly.

Are There Taxes on a 401(k) Rollover?

If you roll over directly from your traditional 401 (k) to a traditional IRA, it is generally not taxable.

However, taxes may apply if:

- Make a rollover to an IRA.

- You’re unable to roll over the funds indirectly within the 60 days.

- You take your money out instead of rolling it over.

- Knowing the tax impact ahead of time can avoid surprises when starting the rollover.

Is Rolling Over Your 401(k) Always the Best Decision?

While there’s no denying that there are great reasons for choosing an IRA, it’s not necessarily the right decision to roll over your retirement before making sure you have examined all the options.

If you are currently employed and happy with your current retirement plan, then it may make sense to leave it in the 401(k). If you plan to retire anywhere between 55 and 59, then there can be additional saving grace from some withdrawal rules in employer-sponsored plans that may not be accessible to an IRA.

What may be the best decision for you really depends on your date of retirement, your investment choices, financial objectives, and tax circumstances.

to an IRA: If you are changing jobs or planning to retire, you may face some important retirement savings decisions){kind=link}